Originally published on LinkedIn, April 28, 2026

The earnings season has come and gone, and broadbrush the South African banking industry has been a pillar of stability and growth;- a national economic treasure! I thought to share some thoughts on strategic direction, but the best arbiter is probably the market.

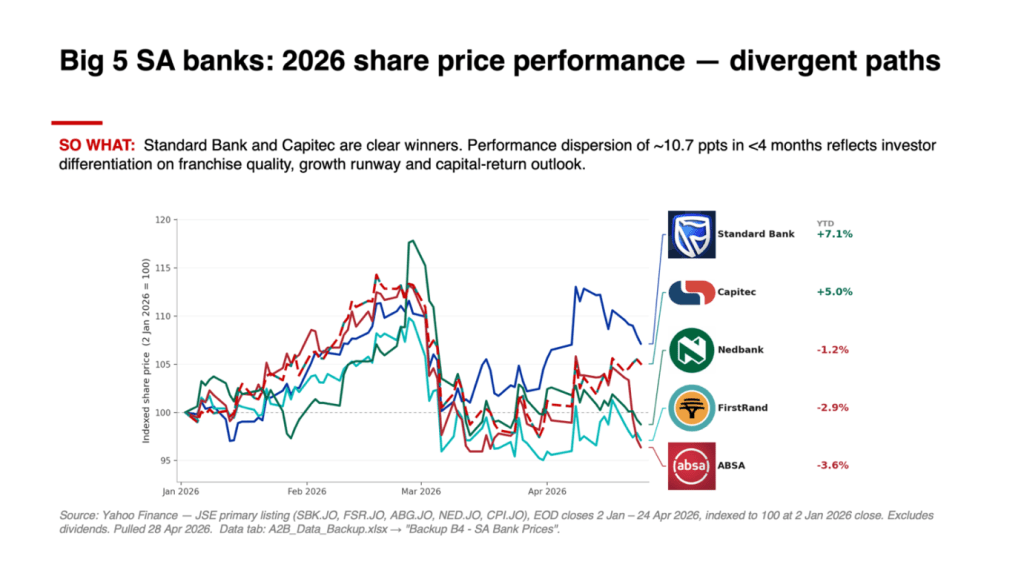

Standard Bank

Standard Bank stole the show and is now not just the biggest bank by assets, but by market capitalization too. This has been achieved through more than just the good results that we see in the rear view mirror. The transparency afforded by their Capital Markets day showed a confidence in their existing strategy to communicate that their commitment to three year 10%pa (midrange) earnings growth projection is a lock (other things being equalish);- which is comforting when your top-rated CEO (and CFO) are retiring in a year. And Sim is still seeing further over the horizon; first in having his C-suite acknowledge the importance of AI and commit to its adoption (astonishing that he and Capitec’s Graham Lee have been the only CEOs to talk to it), and more recently whilst at an overseas conference talking of the likelihood of consolidation in the banking and fintech space. There is a lot happening in a small space. Too much to accommodate everyone. I would speculate that it is not just fintechs and Tier 2 banks at play, especially given the damage wrought by the Capitec Pacman that is rendering the legacy banks subscale (and hurting Insurance companies too). There is probably (allowable regulatory) scope for one big Tier 1 deal for whoever has first mover advantage and has prescoped platform compatibility/integration. If I am a banking CEO right now I would want an AI-advisor at my right hand, and a Corporate Finance specialist gaming scenarios and highlighting opportunities on my left.

Capitec

Capitec continues to disappoint, annual earnings growth plummeting from 30% to 23%. #Firstworldproblems! Sjoe, these guys are good! A few things stood out for me. First, the introduction to their results presentation was an emphasis of culture and purpose and how this has instilled resilience. And because it has been mentioned in every.single.presentation. in the past few years one can be reasonably certain this is not performative. This is real old school “culture eating strategy for breakfast” basics! Second, I have observed a growing tendency for journalists, financial analysts and even banking CEOs to talk about product commoditization and how bank products all do the same thing. Bollocks! Every second slide that Graham Lee presented was a product slide that talked to how it was differentiated in ways that mattered to the customer and new features that had been added. My gut is that most bank CEOs are so far removed from their customers, their frontline and their products, and so myopically focused on dashboard monitors that reflect the jaws of the business, that they have lost sight of what really makes their business tick and succeed, or fail. Too much time with that helicopter view and one forgets what it is like to be on the ground! Capitec is grounded! Third was their take on AI, and the emphasis on worker augmentation. They’ve spent money getting smart people in, but recognize that in a world where digital and AI is a commodity, equipping their people with the right tools will allow for both higher productivity and a better informed human/personal interaction with customers that digital neobanks cannot compete with. Fourth, the growth numbers for Connect (+67% active customers), Funeral Cover Income (+58%) and Business accounts (+71%) are astounding but unsurprising and will underpin growth momentum in the next few years. If there was one item that would scare me (even more) as a competitor, it was the Horizon 3 mention of getting around to Enterprise payments.

Before anyone mistakes me for a Capitec praise-singer, there are concerns. First, I am not sold on Avafin. It is taking too long to find the secret sauce that might make it an offshore winner, and so it is taking too long to scale. This would not have mattered a few years ago. Today, every day that passes makes it more likely that Revolut or some other fintech will have solved for and grabbed the territory. Practically speaking, it may not matter! In the here and now it can be viewed as being a “real option” that unusually (for an option) is washing its own face. The only caution is that if it ever becomes necessary to “pull the plug”, it must be done without hesitation. Second, with the desire to highlight numbers illustrative of high growth, it probably wasn’t ideal to show credit card numbers to higher income (R50k+) individuals up 50% to …15000. Say what! The failure to identify, solution for, target and monetize this segment is astonishing. It is the equivalent of an ultra-efficient low grade gold miner turning their nose up at a high grade deposit. Competitors will be grateful for the breathing space. The same is true of inorganic and acquisitive growth. As much as I have praise for their culture, I have in my head a metaphoric picture of Martin Luther pinning his 95 propositions to the door of the church in 1517 which ushered in the Reformation. Religious adherence to their own dogma/culture (which I praise so highly) is also shutting out earnings accretive opportunities. Be that as it may, even if they are not optimizing on the full opportunity sets at hand, earnings growth will still be substantively higher than competitors until at least 2028 driven by Business and Insurance momentum. And their cost curve positioning means that in most worst case economic scenarios, headwinds would most likely translate to exaggerated market share gains.

ABSA

When I complained of talk of “products doing the same thing”, it was really with ABSA in mind. The new leadership has ticked a lot of strategic boxes correctly with its restructure, new hires and focus on controllable and discretionary costs. And it is understandable that CIB-pros might see retail and business banking through that “commoditised” lens. However, I would recommend that the ABSA Exco (I take that back, make it every bank’s Exco) watch the Capitec financial presentation. My second thought on ABSA is that I am very much sitting on the fence when it comes to the appointment of the previous CE of M-PESA Africa to head Personal and Private Banking. Clearly, Sitoyo Lopokoiyit is a supersmart and capable leader and could not be a bigger tick on the Africa and Fintech strategy side. My circumspection is rooted in a concern that by ticking scale and volume, one might compromise the lower volume, higher value, SA Private Banking/Wealth part of the retail business. It had taken an embarrassingly long time to start pulling the right levers in this space, and hopefully for ABSA that momentum is not now lost in the pivot. Third, I had previously made the comment that it was difficult to believe that ABSAs IT strategy could be leading edge against the backdrop of revolving door CEOs. The R2.4b impairment of computer software lends some support to that view. IT, Platforms and AI integration are going to be crucial in enabling any tactical/strategic rollout – one looks forward to transparency on “where to” from here. The deployment of Salesforce is not a silver bullet. Finally, there is a mischievous question of;- with so many dyed-in-the-wool Standard Bank execs having transitioned to the red brand, if things don’t pan out, it would be a quick and friendly conversation that would see the two come together. Worst case, and needs must!

Nedbank

I still maintain that it is premature to make any calls on Nedbank. There are so many moving parts in its turnaround and the right calls are being made. That said, like ABSA in South Africa, Nedbank has a problem of scale in terms of customer numbers, but theirs is bigger. And until this is put to bed, the existential clock is going to keep ticking.

FirstRand

For sentimental reasons I care a little bit more about FirstRand. And it is definitely racking up more “cognitive dissonance” miles as I try reading the tea leaves. FirstRand itself does not give away a lot. First, the results surprised on the upside. In particular, the performance of FNB, both Retail and Commercial were better than could reasonably be expected given its market dominance. There just should not be that much additional value to be realized from its customer base. Simply brilliant! Then the reason it is almost the worst performing stock this calendar year is the Motonovo debacle. In business, bad things happen sometime that one cannot legislate for, and in this case they’ve been sandbagged by a regulator with political ambition. The additional <R12b fine, loss of future earnings ex- Aldermore/Motonovo plus loss of real option value of a UK asset are enough to explain the loss of relative value. And anyone going “coulda, woulda, shoulda” is being a smartarse post-event. Spilt milk, move on.

Well mostly! There is a common theme to offshore ventures. Ashburton/Jersey was a failure. India was a failure. African operations have been a mediocrity. And pre- the Regulator’s asteroid event, UK operations too were “meh”. Contrast this with the entrepreneurial vigour of Discovery who have seeded/established multiple business lines on every continent barring Antarctica. None have really hit paydirt yet, but it is a helluva portfolio of real options they have. A post-mortem would do no harm.

The FirstRand / FNB Restructure

Turning to the restructure;- the more one looks at it, the more it looks like FirstRand and FNB are consolidating/compacting. There have been successively, more appointments at the FirstRand versus FNB level and more direct reports to Mary (incl Retail and Business Banking, Private Banking and Commercial and Corporate Bank). The FirstRand CEO starts to look like the de facto FNB CEO. It probably makes sense. Organic growth opportunities either outside SA, or in SA in new products or adjacencies, are not immediately visible. So growth must come from acquisitions (and a change in philosophy has been discernible here), and/or earnings growth must come from delayering and cost reduction. Hmm!

I have questioned previously whether the restructuring was customer-centric. The restructured Retail and Business Banking business looks like a straight-up copy-paste of Capitec . Through that lens it is a “hospital pass”. In the past 15 years (i.e. when other boards started to take notice) no banking CEO or Exec has come close to shoring up that segment “beachhead”. And then, to break up the successful Business Banking franchise is helluva risky. It’s fixing something that ain’t broke. And if the primacy of transactional banking in Retail and Business has been the bedrock of FNB success, to have Corporate Banking (with its transactional banking arm) sitting outside of its investment bank does not appear to lean into FNB’s/FSR’s strengths. It is entirely possible that I am being a “when we”, with some misplaced nostalgia compromising my understanding. But I have a sense of unease that I can articulate the strategy and tactics for all the major banks, and the cultural identity for most. I simply cannot do this for FirstRand.

Leave a comment