Originally published on LinkedIn, February 16, 2026

1. Introduction

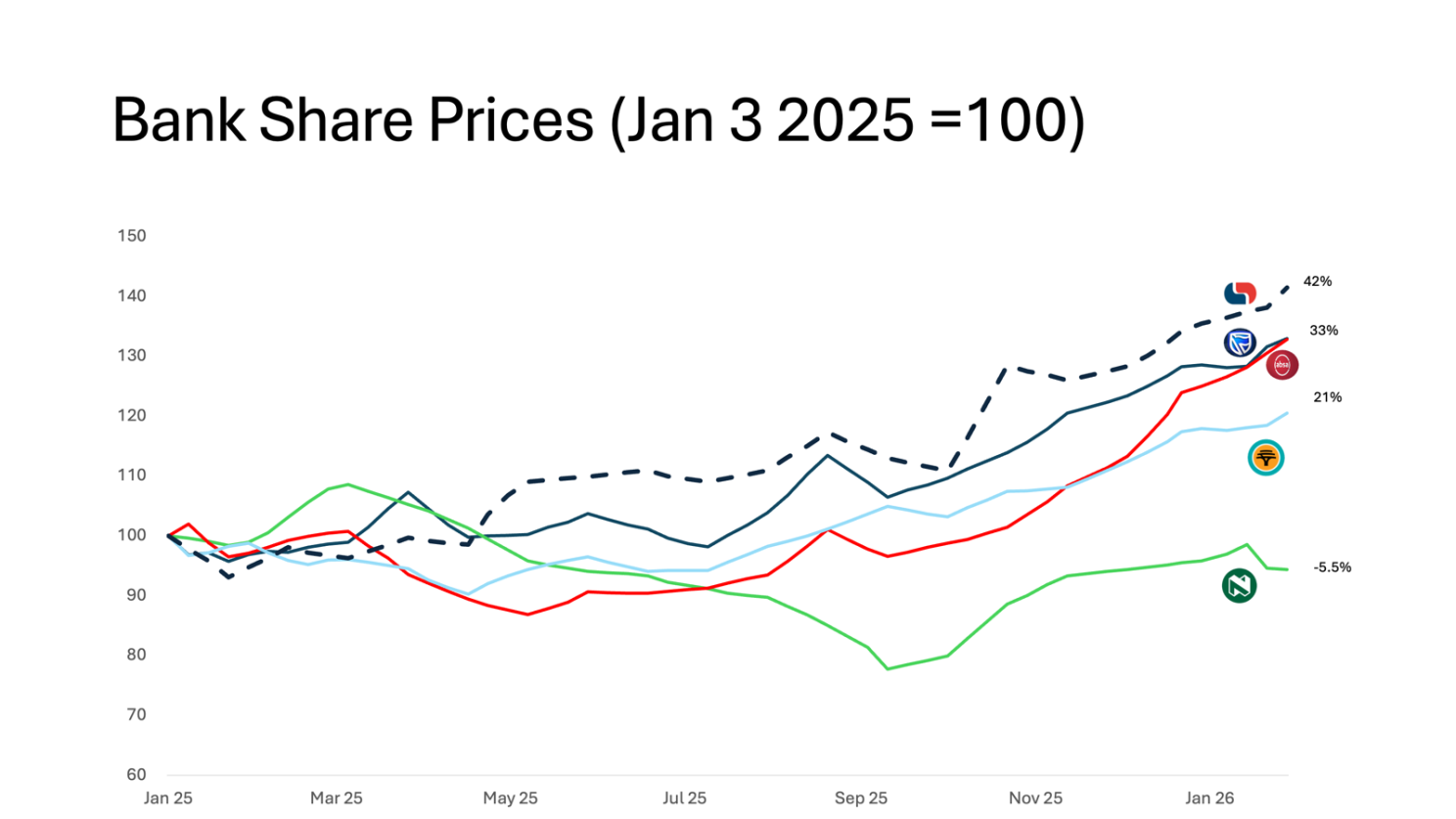

This is the penultimate note in this series on the Big 5 banks. It seems appropriate to have written it up at exactly the same time that Capitec has nosed ahead of FirstRand to be ranked Number One in terms of market valuation.

The series has obviously been an outside-in take, and a mix of insight, analysis, impressions and conjecture. This note is no different. It asks the obvious — “is it worth it”, and looks at some of the “what you need to believes”, a take on competitive differentiators and a brief discussion on “heretical” paths to growth.

2. A Great Business

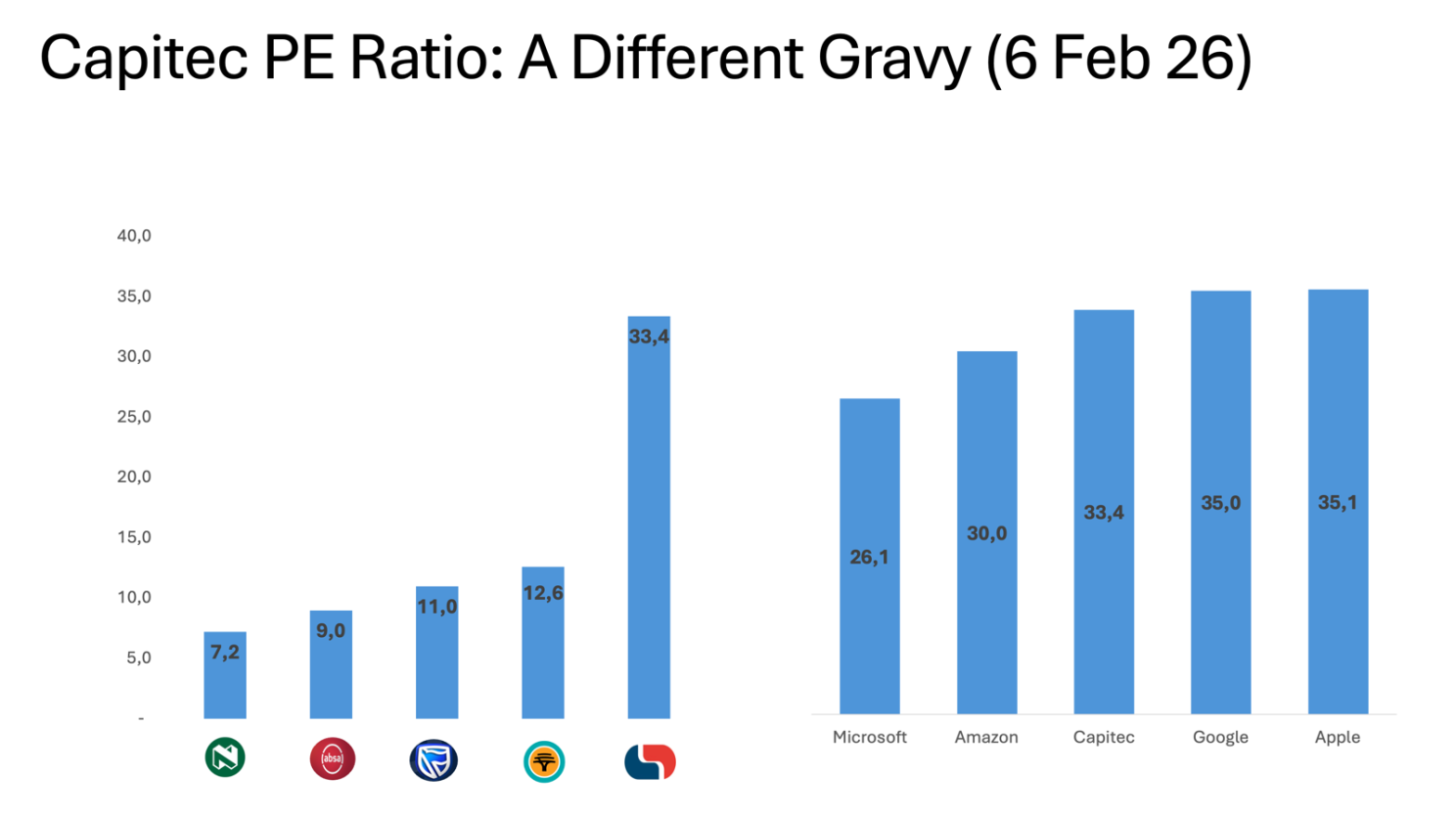

I have no desire to write a panegyric on the success of the “enfant terribles” of South African banking, so let me be done with the obvious; Capitec has been the best run bank — and probably business — in the country! Its Return on Equity (>30%), Cost-Income Ratio (40) and earnings growth rates (>25%) are all at least 10 per cent better than its competitors.

And if you do disagree, you can argue with Mr Market — it’s rated on a different scale to other banks; as highly as some prominent “overvalued” American hyperscalers, and its market capitalisation is equivalent to the entire Life Industry combined (Sanlam, Old Mutual, Discovery, Momentum).

3. But Is It a Good Investment?

Just under a year ago I shared a post; one of the underlying themes being that Capitec might need to do something fundamentally different to support growth expectations. Specifically, that Capitec should look to acquisitions. Since that time, Capitec has done nothing of the sort and is up over 40%. Don’t come to me for stock tips!

It puts me in mind of a Financial Mail article last year (9 Oct), where Simon Brown wrote that “there are broadly two types of investors in the Capitec world: those who own the stock and love it, and the rest, who don’t own it and either hate the stock (because of missed returns) or hate themselves (also because of missed returns)”.

In spite of being so wrong the conviction remains. The reasoning is terribly banal!

First, there is the profit pool dimension. In Consumer Banking the South African profit pool is just north of R45b, and in today’s money, Capitec has about R10b additional upside to capture. In business banking, the South African profit pool is about R30b, of which Capitec might capture R10b if it executes flawlessly (given that customer take-up will probably be greatest in the S of SME and not in medium- and large-sized companies and corporates). And in VAS — specifically Insurance and Connect — one might imagine R5b upside at a tremendous stretch.

None of the above is a given, and is indicative of what rose-tinted perfection and massive good luck might get them to. In the ideal world that still leaves them short of where the Standard Bank Group and FirstRand (normalised run rates of near R45b) are today and they still have the luxury of pulling levers on costs (as ABSA is doing now). The gap is explained by 3 things: balance sheet size, African footprint and having successful Corporate and Investment Banking divisions. The market has made a framing error of confusing excellence in Retail with broad full banking Profit Pool access.

Second is basic math. The math of compounding returns will work against Capitec. Maintaining high growth is a denominator problem. As the base grows, sustaining the same rate requires disproportionate absolute gains — so acceleration demands more “force” each year to stay constant. To illustrate frivolously; in its last 3 presentations, year-on-year earnings growth has “plummeted” from 36% to 30% to 26%. And the trading update that has just been provided for the full year suggests the earnings number will be in a range of 20-25%. This is brilliant, but lower still! The tyranny of the second order derivative!

4. Observations on Competitive Differentiators

a) Leadership (Operational excellence > Bean Counters): With the “Legacy 4”, you will observe that the greater part of presentations (and Analyst questions) are devoted to the economy, credit cycle, endowment hedging, interest v non-interest income, C:I, ROE, COE, NAV and so on — the full suite of the most important metrics needed to simplify the management and measurement of huge businesses. When you watch a Capitec presentation you get a rapid-fire presentation on the business itself. Leadership clearly know what is going on with their company and are not managing by instrument panel. They are intimate with the nuts and bolts and do not suffer from “x degrees of separation” from the operations.

b) Culture: That old chestnut of “culture eats strategy for breakfast” is perhaps too glib and overused. But Capitec’s got it right with its behavioural values of “ownership, energy and client first”. And these are entrenched in the onboarding process. This is very similar to the onboarding process at FirstRand in its early days when the “founders” themselves would walk you through the how’s and why’s of an owner-manager culture. Two totally different approaches, but both unlocking human agency at the outset and embedding a “why”.

c) Staff Costs: In FY2025, Capitec’s unit staff costs rose a substantial 25% (to R570k/employee). This was a result of higher incentive/bonus payments, a higher minimum wage and the targeted recruitment of IT, Analytic/ML smart people. In spite of this increase, the unit staff cost was still only 60% of that of the average of the Big 4.

d) Digital v Human: The speed of transition to a new tech stack (so that people transitioned from building systems to building products) and effectiveness in supporting sales, service and new product rollout, are indicative of Capitec having a leading digital capability. This matters in our new neobanking, digital-only, fintech world where “OMG AI is coming”. Nothing is more important than digital proficiency.

Nothing that is, other than people and human connection. There is a reason that Capitec keeps expanding its branch footprint whilst other actors’ “right size” theirs. High touch coexists with high tech. Digital is an enabler. But a human connection provides: a trust anchor because one person is looking you in the eye and taking ownership, empathy when things go wrong, hand-holding when you do something for the first time, an opportunity to educate, and a much better chance of advising and selling to a need.

e) Low Risk Market Entry: Every time Capitec enters a new market segment, its success is guaranteed. This is by design. It knows the market, understands what it needed, and has proven the concept before it starts. With its transactional offering, Global One was based on a detailed understanding of Capital One’s monoline offering. With Insurance it first operated with “cell captives” before getting its own licence. In Business banking, Capitec first bought Mercantile Bank in 2019. With homeloans, Capitec collaborated with SA Homeloans as an originator before taking loans onto its own balance sheet. Failure is almost impossible.

f) AI and Data Analytics: A year ago I ran a wordcount exercise on annual presentations by Bank CEOs to ascertain whether AI was a top-of-mind agenda item. It was disappointing. I ran the same exercise over the latest presentations, and found incredibly, it was possible “to fall off the floor”. AI was mentioned a total of zero times by the Legacy 4 banks. It was mentioned 19 times by Discovery and 4 times by Capitec. This pretty accurately reflects the respective state of advancement and AI capability by institution.

5. Growth Vectors

Business-as-Usual: There is no reason why Capitec’s entrance into Business Banking should not be successful. It is a copy-paste analogue of a proven formula. This is especially true of the S in SME. Standard, ABSA and Nedbank have already been wobbling in the business space so the emergence of a low cost, innovative, proven success will be giving them sleepless nights.

Heresy 1 — Private Banking is an option: Tax tables from 2023 reflected that under 10% of taxpayers earning over R750k contributed just under 60% of personal income tax. There is merit to a Pareto analogue that a small number of Private Banking customers probably make up over half of the Consumer Banking profit pool. It is surprising that Capitec has not been more targeted. It is not difficult to design a stand-alone product, with a price point much lower than the R600 entry level for typical Private Banking.

Heresy 2 — Balance Sheet lite is not enough: December BA900 returns show Capitec represents less than 3% of the banking sectors’ Total Asset (lending) base of R8.9b. Homeloans are an obvious starting point. A cost-efficient player with a credit pricing edge should have the ability to build a balance sheet more assertively.

Heresy 3 — Avafin will not be Capitec 2.0: Other than being digital only, Avafin looks very similar to early Capitec. The challenge for Avafin though is the new breed of competitor that has emerged from nowhere; Nubank in Latin America and Revolut in Europe. These two banks are in a race to scale, the pace of which is unlike anything ever seen before in banking. Size will matter in the balance sheet and brand trust game.

Heresy 4 — Low Risk organic market entry is not enough: Inorganic growth offers the best path to a step change in earnings growth. Capitec has a unique opportunity to become a paper tiger and dominant, based on its premium market rating! Everything else seems cheap, and earnings-accretive. This opportunity may never present itself again.

6. In Conclusion

Along the way, this note turned into a tome. The thread though is simple. Capitec is the best business and most efficient product factory in South Africa. Everyone associated with its success should feel a massive sense of pride. That said, even with rose-tinted spectacles, it remains a challenge to justify its market valuation. There are new competitors emerging, and it will be a stretch to attain earnings parity with the biggest of its competitors, FirstRand and Standard Bank. This might be mitigated if some growth vectors are given more focused attention and Capitec opportunistically responds to the options its paper valuation allows.

That said, it would be remiss of me not to be explicit that I have been consistently wrong both about Capitec as an investment and what is operationally achievable. They will be very comfortable swiping left!

Leave a comment