Originally published on LinkedIn, January 2026

1. Introduction

The best “Business Unit” in African (not just South African) banking is Standard Bank’s Corporate and Investment Banking division. It is as completely dominant as the South African forward pack.

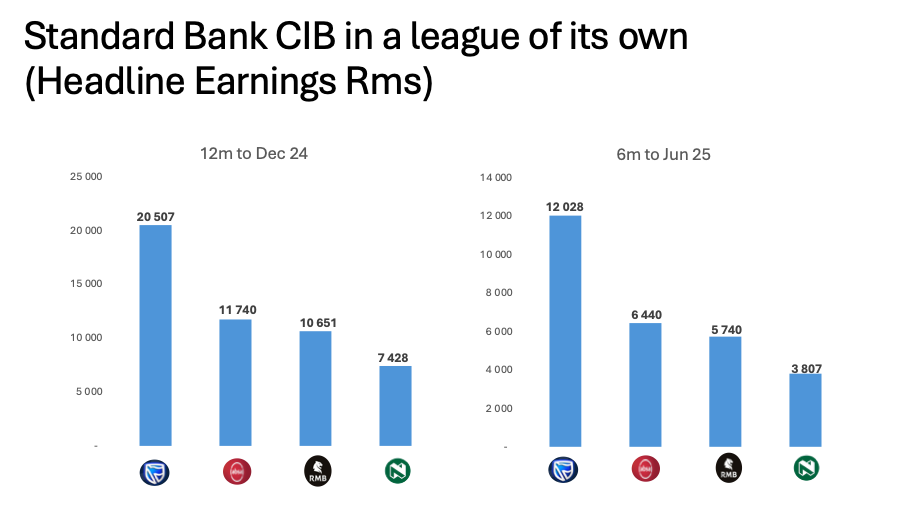

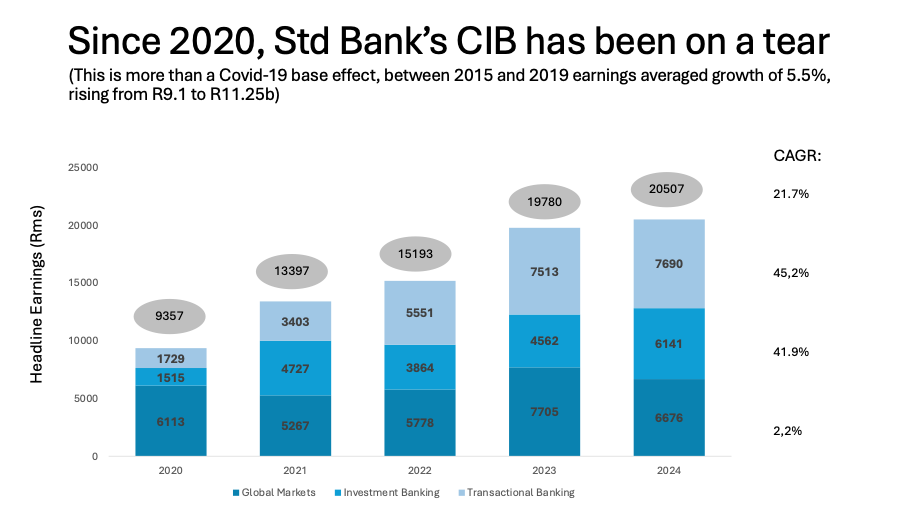

In the latest available 6 month reporting period it generated headline earnings of R12b. This is more than ABSA (R11.87b), and almost 50% more than both Nedbank (R8.4b) and Capitec (R8.0b). Think about that. One high growth BU generating 50% more than Capitec, which itself is valued more highly than the whole of Standard Bank?! Efficient markets and all that!

Unpacking the reasons for this success is challenging without visibility “under the hood”. The availability of data is only outweighed by the opacity of said data and generality of public domain commentary. It would be stupid to share your “secret sauce”. Nonetheless, a few conjectures have been set out below that will hopefully stand scrutiny. Feel free to let me know what you think is BS (and why)!

There are four reasons posited for SBK’s CIB success: Leadership, African dominance, Market-making dominance reinforcing itself through a network effect, and leveraging partnerships.

2. Leadership

The Springboks have Rassie and Siya. Standard Bank have Sim. I see a very strong correlation between great leaders and great performing companies. My go-to examples have tended to be Adrian Gore and Gerrie Fourie. With Gerrie Fourie standing down, one figure towers (metaphorically) over the others amongst the Big 5 banks, and that is Sim. At every presentation I see and hear a Level 5 leader. What do I mean by this?

A level 3 leader — a competent manager — organizes people and resources to achieve objectives, plans, budgets and creates systems and processes to deliver results through efficient execution. This is the minimum baseline for SA bank execs. A level 4 — or effective — leader sets a vision and strategy, makes hard decisions and leads change and growth. ABSA and Nedbank have literally had to bring in leaders from the outside to initiate this. As per my last note, FirstRand is starting to make progress in its evolution, though its culture, vision and strategy remain opaque. A level 5 leader — an elite Executive — focuses on long-term institution building via succession planning, entrenching culture and building capability. And this is centered around a “why”. The strapline for Standard Bank — Africa is our home, we power her growth — has been at the heart of SBK’s and SBK CIB’s growth in the past decade. From the outset, Sim has been consistent. If there is a clarity in what and where Point B is and why you want to get there, it is a helluva lot easier to get there!

3. Africa

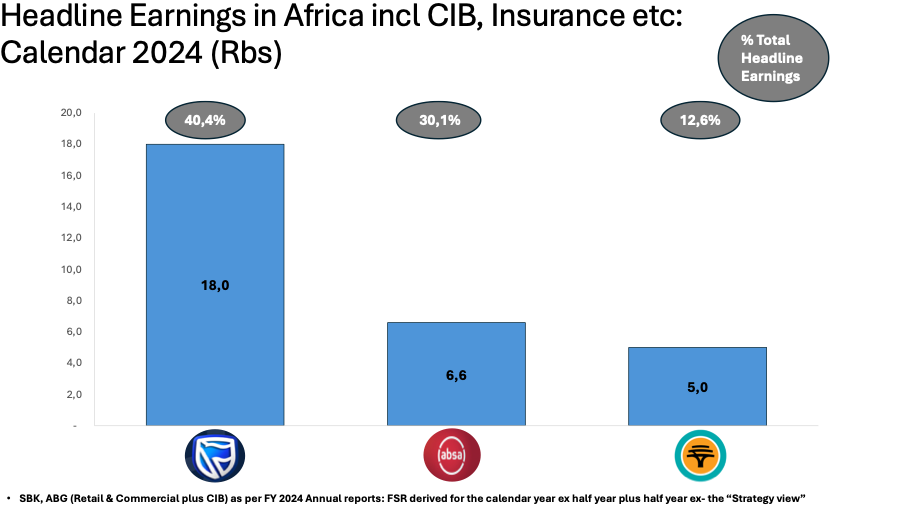

A while back I penned a note questioning why SA banks even bother with Africa. The basic premise was that Capitec makes just about as much selling funeral policies in SA as FirstRand and ABSA do in Retail and Commercial banking in 10 or so African jurisdictions (half that of SBK). Standard Bank’s CIB offers the rebuttal.

To revisit that story. The top performer in Africa was Standard Bank. Its Retail and Commercial banking operations in Africa generated R2.8b. Not much more exciting than the R1.5b+ ex-ABSA and FSR. BUT, total African headline earnings were R18b. The total generated by CIB was probably not as much as the full R15b difference. Cost allocations ex the centre, insurance losses, ICBC offsets and accounting “sleight of hand” probably reduced total CIB earnings ex-Africa to about R12b. But that is huge! It is at least 4x the amount generated by its conventional banking activities.

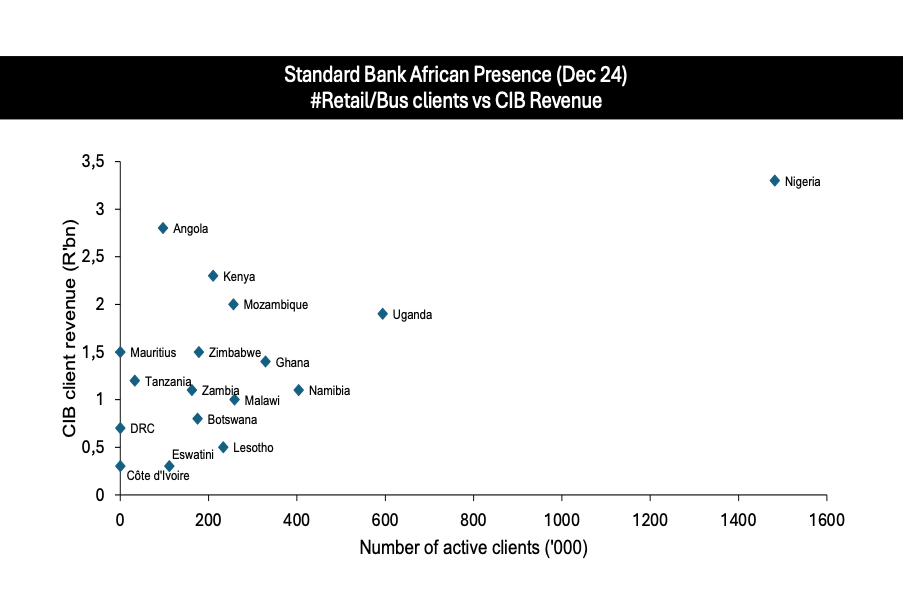

And what that means looking at Standard Bank’s African portfolio is that the x-axis is substantively irrelevant. When one shouts “show me the money”, Africa is a y-axis (Corporate and Investment Banking) game.

Don’t get me wrong, conventional banking has 3 benefits: presence and relationship-building, a local currency balance sheet to lower the cost of local funding and significant (700bps) interest margin benefits. (NIM in Europe tends to 160bps; SA tends to 300 to 350bps — remarkably similar to the difference between prime and the repo rate). But profit in conventional banking barely moves the needle.

Having a presence in double the number of jurisdictions as its competitors is a non-trivial advantage from a portfolio perspective. Although GDP growth prospects in Africa (>4%) are much better than in South Africa on average, the risk associated with individual countries has tended to be higher. But just like with stock portfolio construction, the more countries the less the risk for the overall portfolio. In 2024 for example, there were massive currency devaluations in West Africa. But the rest of the portfolio offered stability. Similarly, in 2025, CIB will take hits in Mozambique and Malawi. But the 50% rebound in West Africa (H1 2025), together with growth elsewhere will see continued double digit growth of the African CIB portfolio.

4. Market-Making and Network Effects

If you are a multi-national or large corporate, you need access to foreign exchange, for exports and imports, to move money between countries, the ability to hedge, and the ability to raise finance. You will need two things, a common presence in your multiple markets — by virtue of its much wider presence SBK is most likely to tick that box, AND you need a market maker in forex. Standard Bank has more than just a presence. It is a market maker in almost all of its functional areas. But in forex, it is more, it is top ranked in at least 10 of the jurisdictions in which it operates, and at least Top 3 in the balance. This is true in South Africa too. I recall hearing someone in CIB relating that 60% of ZAR trades were done by SBK. This is a serious competitive advantage. It is the equivalent in Retail or Commercial banking of having the primary transactional account. You get first dibs on everything else: transactional banking, equity raises, debt funding, investment and cash management, Treasury support. You literally just have to show up with the necessary industry and functional expertise, together with a supporting platform and you are through the door. This is the power of the network effect. And no-one compares to Standard in leveraging this.

To be a market-maker is non-trivial. You have to offer a bid price (what you’ll pay), an ask/offer price (what you’ll charge to sell) and provide liquidity. In doing this you run the risk of unintentionally establishing a long or short position, and in the event of a significant adverse event, can lose a huge amount in almost no time. Standard Bank CIB has not experienced anything like this. Whoever the team is in Treasury that manages their Value-at-Risk deserves (and I am sure receives) massive bonuses. I doubt there is a more important risk management function, not just in CIB, or Standard Bank, but in corporate South Africa.

In terms of industry expertise, you tend to hear the same from all SA’s banking CIB arms. They all have deep expertise in important industries, financial services, mining, telecoms, consumer goods. Standard explicitly talks of African development and growth being underpinned especially by the need for Infrastructure and Energy. Common sense really! But their numbers in 2025 are backing it up. I go to the biggest mining event in Africa — the Mining Indaba in Cape Town. Who has the biggest presence and stands out, Standard Bank. I go to the biggest agricultural show in Africa, the NAMPO exhibition in the outskirts of Bothaville, who has the biggest presence and stands out, Standard Bank. They have literal presence and “boots on the ground”.

5. Partnerships

Before China became the second superpower it is, Standard had partnered with it in Africa via ICBC. The China-Africa trade corridor was and is a rich resource if you can tap into it. Is this going to change? The Financial Times published a report showing China’s belt and road initiative spending almost doubled to $213b in 2025. A big chunk of this spending growth was directed at energy exploitation (ie coal, oil and gas). In the crazy geopolitical environment we are experiencing, almost every economic actor is being driven towards better trading relations with China. By becoming the first African bank to offer international transactions through China’s cross-border interbank payment system (CIPS), Standard Bank has positioned itself to take further advantage of a proven and possibly accelerating growth vector.

Another growth vector being unlocked by a combination of own deliberate economic resource redirection and the “blossoming of relations” with the United States in particular, is the Middle East. Most of the Gulf states are working to a version of Saudi’s Vision 2030, a common sense initiative to reduce dependence on oil by diversifying economies and investment holdings. We’ve seen this most recently with the MBO of Barloworld funded by Saudi’s Gulf Falcon Holdings. This makes the opening of a rep office in Egypt especially interesting. I am not certain that it is a natural part of the pipeline of capital flows from the Middle East to Africa. Dubai and/or Saudi itself might be better positioned. But it is the first presence of a South African bank in North Africa.

6. The Future

Being Number One, and staying there, are two completely different things. The scale and diversity of SBK CIB’s position and offerings represent a reinforcing network effect that makes them seem impregnable. But the competition is not sleeping. SBK was seen as a shoe-in to take over Kenyan-based NCBA. And then Nedbank swooped in. Was this a surprise? The fact that SBK felt it necessary to have a press release confirming East Africa and Kenya were important to them suggests yes. ABSA have been even more direct, poaching several top CIB-related Execs, not least of whom is their new CEO. Sport is a great metaphor for life, you’re as good as your last game. As it stands though, the competition in Corporate and Investment banking has a lot of catching up to do.

Leave a comment